Solana Payments: The Fastest-Growing Payment Layer in Crypto

$2 Trillion in Volume, a World-Class Partner List, and One Question That Remains.

BY VICTOR · MR. Z

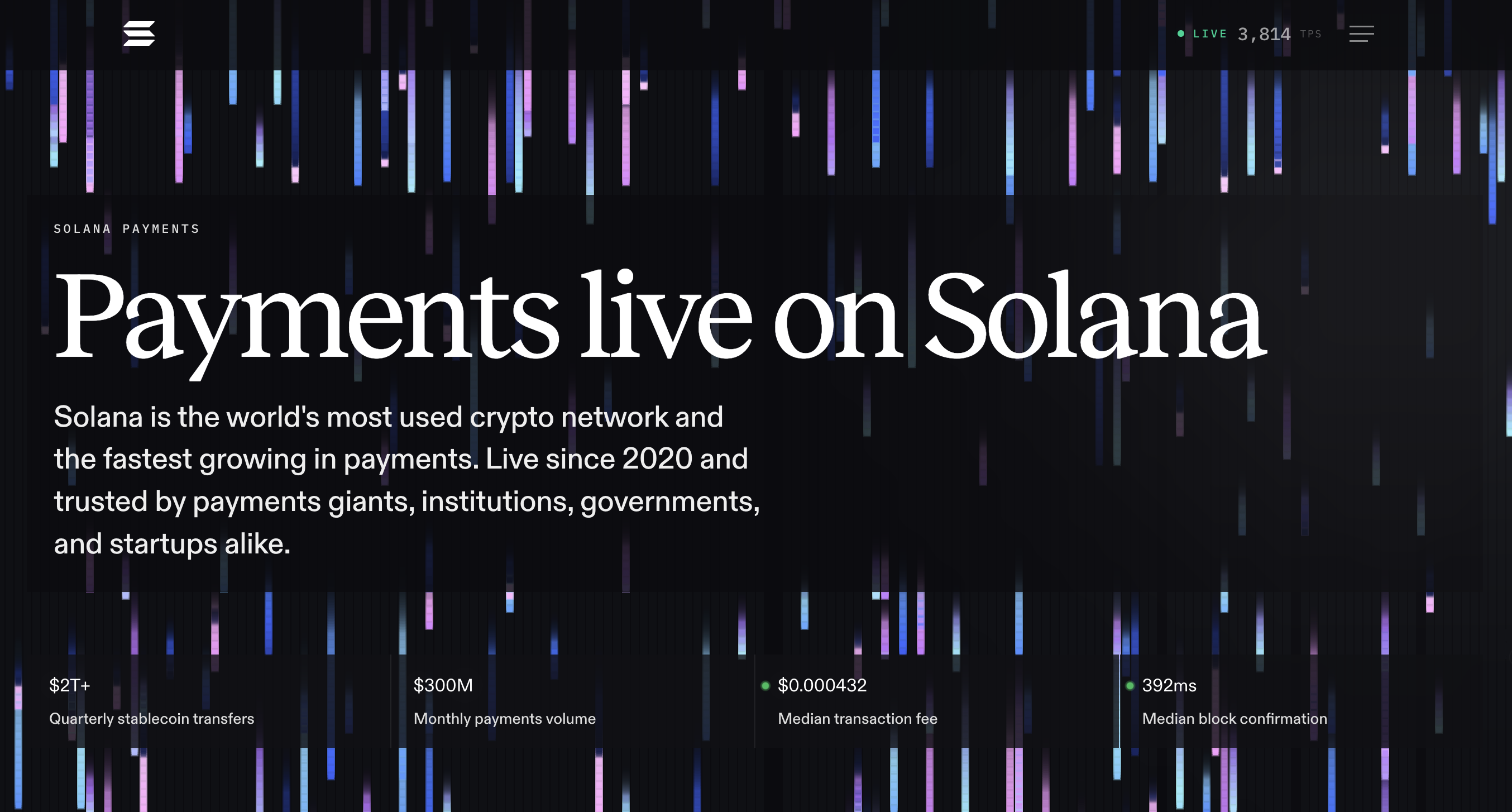

On February 26, 2026, the Solana Foundation launched payments.org.

No token launch, no liquidity incentive — just a payment infrastructure portal: a mainnet live transaction simulator, developer documentation, institutional case studies, and a set of numbers that are difficult to ignore.

755.3% year-over-year TPV growth. Over $2 trillion in quarterly stablecoin transfer volume. Visa, PayPal, and Western Union in production deployment on the same network.

The data tells a compelling story. But how much of it reflects durable, organic demand?

This report is produced by 168X (@168X_Fortune), a research and investment platform at the intersection of Eastern and Western capital markets, covering AI, Blockchain, Robotics, Space Technology, and Biotech. Hosted by former banker Mr. Z (@168MrZ).

Key Findings

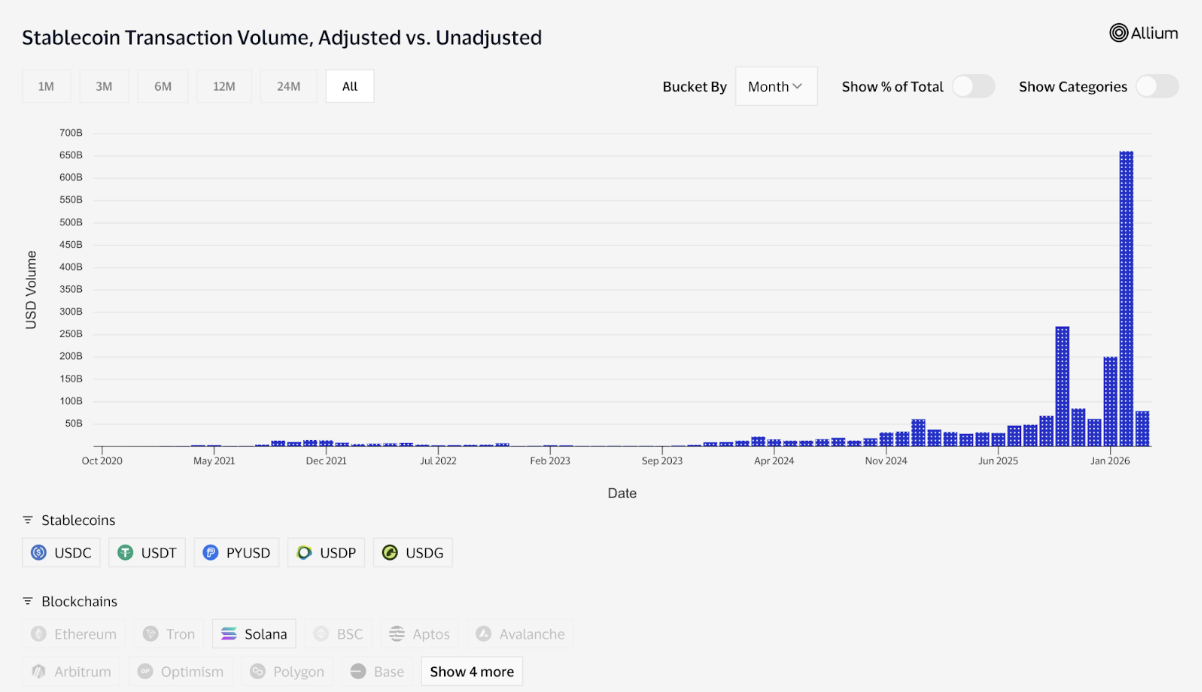

- Solana's quarterly stablecoin transfer volume has surpassed $2T, with annual TPV growth of 755.3%, far exceeding the fintech peer median of 268%

- Institutional adoption is in production, not pilot: Visa, PayPal, Stripe, Western Union, and Fiserv have all deployed on Solana at scale

- Despite strong headline metrics, Tron dominates real-world stablecoin payments by volume; Solana's retail-level transactions account for ~1% of its total on-chain activity

- Agentic payments (AI agent micropayments via the x402 protocol) is Solana's clearest differentiated thesis, but 78% of peak-period activity was classified as non-organic

- The central investment question: can Solana convert institutional infrastructure into sustained, organic payment flow at scale?

I. Strategic Context: Where Solana's Payments Ambition Began

Many assume Solana's payments push is a new story from 2025. In fact, it traces back to 2022.

- February 2022: Solana Labs launched Solana Pay, the first decentralized, permissionless payment rail allowing merchants to accept stablecoins like USDC at near-zero fees. That same year, FTX collapsed, SOL dropped from $260 to $8, and the entire ecosystem's credibility nearly evaporated. Solana Pay launched into the void, largely unnoticed.

- August 2023: The turning point. Solana Pay integrated with Shopify, giving millions of merchants the ability to accept USDC.

- September 2023: Visa selected Solana as one of its blockchains for expanding stablecoin settlement. That December, Circle launched EURC natively on Solana.

Connect the dots, and Solana's strategic path has been remarkably consistent:

Solana Pay (2022) → Shopify Integration (Aug 2023) → Visa Selects Solana (Sep 2023) → PayPal Launches PYUSD (2024) → Stripe Acquires Bridge with Solana as Settlement Rail (2025) → Western Union Launches USDPT (2026) → payments.org Goes Live (Feb 2026)

On February 26, 2026, the Solana Foundation launched payments.org: not a token launch, not a liquidity incentive, but a payment infrastructure portal featuring a mainnet live transaction simulator, developer documentation, institutional case studies, and production-grade metrics. The launch is a public declaration of this four-year strategic build.

As Sheraz Shere, Head of Payments and Commerce at the Solana Foundation, put it: "We've reached the stage of the innovation cycle where genuine use cases are starting to take shape."

II. The Big Picture: Solana Payments by the Numbers

- Quarterly stablecoin transfer volume: $2T+

- Monthly payment transaction volume: $300M+

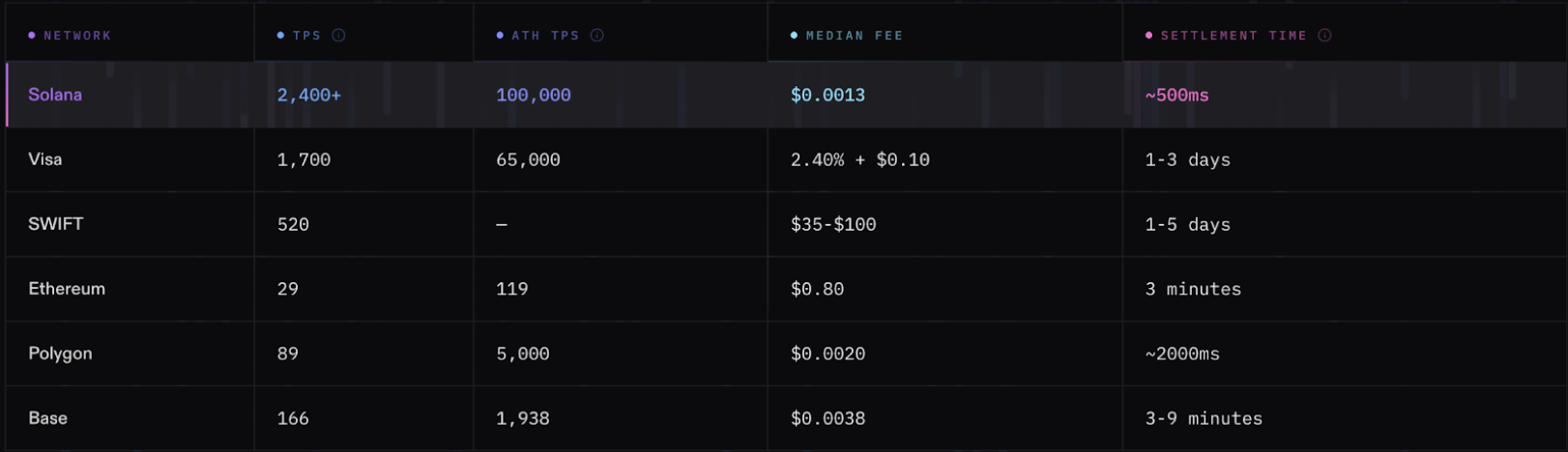

- Median transaction fee: $0.000437

- Median block confirmation time: 392ms

- Daily transactions: 70M–100M+

- Annual TPV growth rate: 755.3% (vs. fintech peer median of 268.24%)

Solana's daily transaction volume now surpasses the combined total of BNB, Ethereum, and every other blockchain, while maintaining roughly 10x the real TPS of competitors at the lowest median fees in the industry.

Traditional financial institutions have moved beyond pilots into production-grade deployment. Visa and Worldpay use Solana for USDC back-end settlement. PayPal deployed its native stablecoin PYUSD on Solana, reaching hundreds of millions of users and tens of millions of merchants worldwide.

These partnerships validate Solana's enterprise-grade reliability while generating meaningful transaction flow and ecosystem network effects.

III. Deconstructing the $300M/Month: Who's Actually Using Solana for Payments?

Solana's monthly payment volume is not attributable to a single application. It reflects a diversified ecosystem across multiple verticals.

3.1 Crypto-Native Payment Platforms

- Helio (owned by MoonPay) is the single largest contributor, with an annualized processing volume of approximately $1.5B (roughly $125M/month), accounting for around 40% of total payment volume. It primarily serves e-commerce and NFT marketplaces, connecting over 6,000 merchants and 450,000 active wallets.

- Stripe / Bridge achieved 400% volume growth in 2025, with Solana serving as its primary stablecoin settlement rail, particularly for USDC-denominated cross-border payroll. After Stripe's $1.1B acquisition of stablecoin orchestration platform Bridge, the full "fiat-in → stablecoin settlement → fiat-out" loop is now in production. Businesses can accept local currencies, settle via stablecoins on Solana, or batch-pay directly from on-chain wallets to traditional bank accounts.

3.2 Enterprise Treasury and B2B Infrastructure

- Squads provides multi-sig and treasury management tools securing over $10B in assets. Enterprises increasingly use Solana stablecoins for vendor payments and financial settlement.

- Sphere, a cross-border payments platform, processed over $100M in the past year, supporting instant settlement from crypto to bank accounts.

- Huma Finance saw transaction volume surge 232% in 2025 to $8.9B. Following its merger with Arf, the combined entity now replaces traditional SWIFT flows with 24/7 stablecoin settlement.

3.3 Consumer Payments and Card Ecosystem

- Kast launched a Solana stablecoin debit card, with 10,000+ cards issued and acceptance at over 100 million merchants globally. In February 2025, Kast partnered with Gauntlet to launch KAST Earn vaults, offering 4–9% stablecoin APY, with funds earning yield until the microsecond before a purchase clears. This architecture makes spending and yield generation a single, simultaneous action — structurally impossible with traditional debit products.

- Revolut (Europe's largest neobank, 65M users) added full Solana network support in December 2025, enabling over 15 million crypto users to transact in SOL, USDC, and USDT.

- Sling operates in 140+ countries, supports instant bank withdrawals in 75 countries, holds EU MiCA and UK FCA licenses, and is integrated into Mexico's SPEI system.

- In February 2026, Noah embedded compliant banking infrastructure into the Jupiter super-app, giving 50M+ users access to virtual USD and EUR accounts.

3.4 Production-Grade Deployments by Traditional Finance Institutions

- Visa: USDC settlement annualized at $3.5B+; internal reports note "Solana has the potential to become one of the networks powering mainstream payment flows"

- Worldpay: Runs its own Solana validator node; uses USDG to reduce processing times by 50%; 57% of all USDG issuance is on Solana

- PayPal: PYUSD market cap on Solana reaches $835M, up 500.9% YoY, with distribution to 400M users and 30M merchants

- Fiserv: Issued FIUSD institutional stablecoin using Token Extensions for regulatory compliance controls

- Western Union: USDPT to connect 360,000+ global cash pickup locations across 200+ countries

- Gusto: Beginning January 2026, delivering instant USDC payroll for 400,000+ businesses

Solana's payments ecosystem now spans the full spectrum from crypto-native infrastructure to major traditional financial institutions.

IV. The Stablecoin Battlefield: Why Solana Aligned with USDC

Solana's stablecoin ecosystem has a clear structural profile: USDC dominant, USDT secondary, PYUSD emerging.

As of early 2026, Solana's stablecoin supply sits at approximately $14B (4.5% of the global stablecoin market), nearly tripling from $5B at end of 2024. In circulating USDC, Solana ranks second globally, behind only Ethereum. In February 2026, Solana recorded $650B in stablecoin volume in a single month, more than double the previous record set before October 2025 and the highest monthly figure ever achieved by any blockchain.

Grayscale Research noted that on-chain activity on Solana is shifting from memecoin-driven DEX trading toward SOL-stablecoin trading pairs, representing a structural rotation from speculative to utility-driven flow. Standard Chartered confirmed the same trend independently.

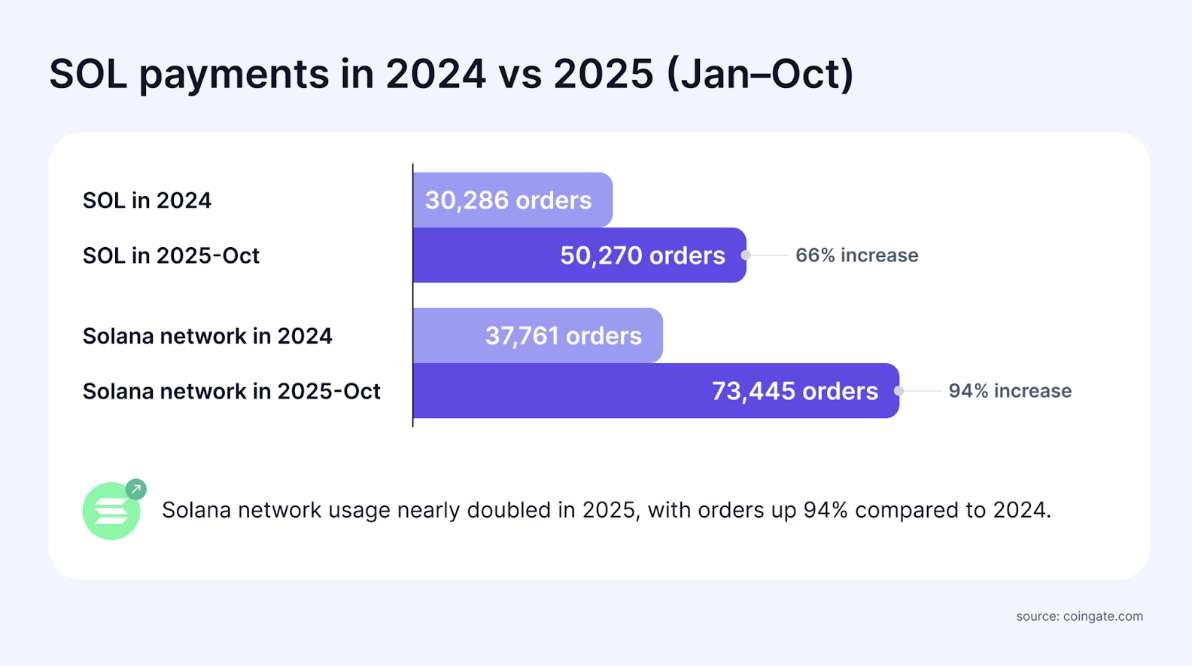

Real consumer data from CoinGate, a European crypto payment processor with 100K+ merchants and approximately 1–1.5M annual transactions, provides granular ground-level context:

- Solana network payment composition: 68% SOL, 28% USDC, 4% USDT

- SOL payment transactions: +66% YoY; total Solana network payments: +94% YoY

- SOL ranks 7th across all CoinGate payment currencies at 6.8% share

- Solana network peaked at 8.4% of total CoinGate site volume in September 2025

The implication: Solana is positioning itself as the high-frequency settlement layer for USDC. The USDC + high-performance chain stack is now the standard architecture for payment applications including Stripe, Helio, and Sphere.

The Solana Foundation has reinforced this institutionally:

- Institutional Toolkit addressing compliance requirements including tokenization, AML, and KYC

- Token Extensions providing institutional stablecoins (Worldpay's USDG, Fiserv's FIUSD, PayPal's PYUSD) with asset freeze controls, transfer restrictions, and confidential transfer capabilities

- All top 10 global stablecoins now natively issued on Solana

V. CoinGate Data: A Ground-Level View of Consumer Payment Behavior

CoinGate provides consumer-side data, distinct from institutional metrics. A closer look reveals where organic retail demand actually concentrates.

User Geography: Europe 36.9%, Americas 36.1%, Asia 15.4%. Distribution is relatively balanced with no single-market dependency.

Top Industry Verticals: Web hosting and domain services 35.5%, consumer goods and services 11.8%, computer-related products 9%. The largest single merchant is Hostinger (30.4%), followed by IPRoyal (5.3%) and CoinGate Gift Cards (5.2%).

The pattern is consistent with broader crypto payment adoption dynamics: Solana's consumer payment penetration has first taken hold in subscription-based, digital-native, and utility-type spending: hosting, VPN, proxy, and IT tools, rather than physical retail. Digital-native contexts have the lowest integration friction and represent the natural initial penetration point for crypto payment rails.

Transaction Size Profile: Average order value in 2025 was approximately €50. Transactions ranged from €0.12 to €14,019, with one notable outlier: a 169 SOL (~€30,957) single transaction for proxy services. Solana's fee structure supports the full range from micropayments to large-value transfers within a single network.

VI. Competitive Landscape: Tron's Structural Dominance in Stablecoin Payments

Solana's headline numbers are strong, but a full-picture view of global stablecoin payment flows tells a more complex story.

A 2025 deep-dive report on stablecoin payments by Artemis and Dragonfly did not include Solana among the "mainstream settlement chains."

By transaction volume share: Tron first, Ethereum second, then BSC and Polygon.

Regionally, Solana has minimal presence in the current stablecoin payment landscape:

- North America and the Caribbean: Tron / Ethereum dominant

- Europe / Africa / Latin America / Asia: Tron leads in most countries, Ethereum consistently second, BSC/Polygon hold share in select markets; Solana is not a significant factor in any major regional flow

Tron's structural advantage is straightforward: lowest fees, USDT ecosystem dominance, and deep penetration across emerging markets. For remittance users in the Philippines, Nigeria, or Brazil, the decision framework is simple — lowest transfer cost wins. Tron's USDT has built deeply entrenched behavioral habits in these markets that are difficult to displace on technical merit alone.

An additional data point reinforces the gap: Solana's retail-level transactions account for approximately 1% of total on-chain volume. The remainder is dominated by exchange clearing and large institutional fund movements. Everyday retail payment use at the individual consumer level remains statistically marginal.

This clarifies Solana's actual positioning: closer to an institutional settlement layer and emerging payment infrastructure rail than a mass-market remittance network. The two serve fundamentally different user profiles, technical requirements, and compliance needs, with minimal competitive overlap. Recognizing this distinction is essential context for evaluating Solana's incremental growth opportunity.

VII. Agentic Payments: Solana's Differentiated Thesis

If Tron owns the established stablecoin remittance market, Solana's incremental narrative points to an emerging frontier: Agentic Payments.

7.1 The Structural Opportunity

AI agents can already write code, scrape data, and deploy resources autonomously, but whenever a paid API or external service is required, the workflow still depends on humans to create accounts, configure payment methods, and provision API keys. These manual dependencies are the primary friction points in AI-automated pipelines.

Agentic payments addresses this directly: on-chain micropayments enable AI agents to autonomously send requests, complete payments, and continue executing tasks, without accounts, API keys, or human intervention. The technical requirements are sub-cent fees and sub-second settlement — precisely Solana's core performance parameters.

7.2 The x402 Protocol

x402 leverages HTTP's native 402 Payment Required status code to enable payment negotiation between clients and servers within standard web architecture, requiring no new protocol layer.

Transaction flow: Client requests API → Server returns payment conditions → Client attaches signed payment → Facilitator settles on-chain → Server returns data.

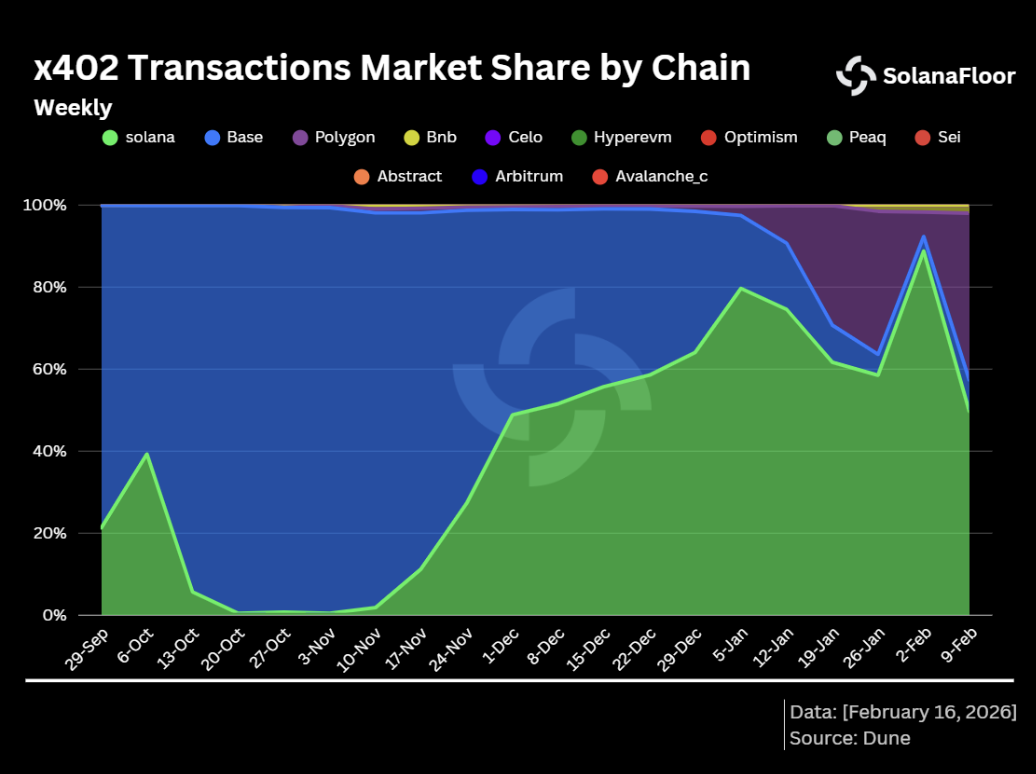

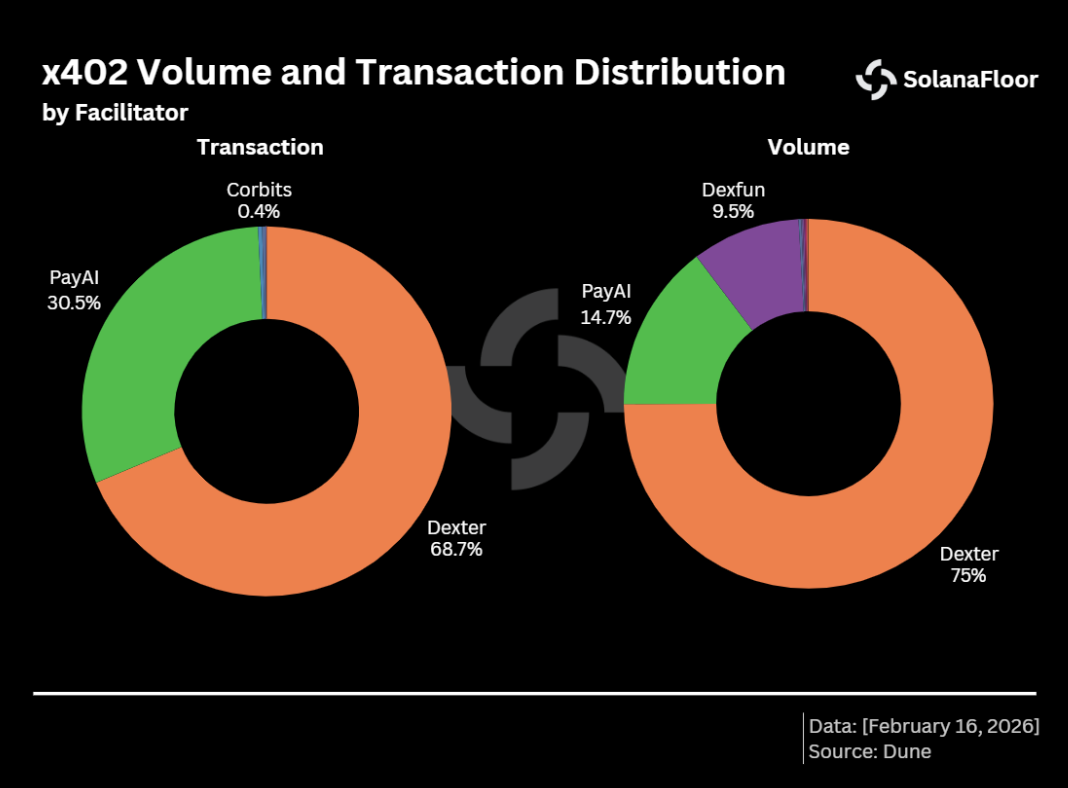

Cumulative on-chain x402 activity to date: 120M+ transactions, with total transfer value exceeding $41M. Base has accumulated approximately 70M transactions ($21.5M); Solana approximately 45M transactions ($16.4M).

7.3 Momentum and Risk Factors

Despite trailing Base in cumulative volume, Solana's recent growth rate is faster. In the week of December 8, 2025, Solana recorded 5.8M transactions vs. Base's 5.3M, briefly capturing 88% of total x402 transaction share in early 2026.

On Solana, two facilitators handle the majority of activity: Dexter (68.7% of transactions, 75% of volume) and PayAI (30.5% of transactions, 14.7% of volume). Facilitators function analogously to Stripe in card payments, collecting micropayments on-chain on behalf of API service providers.

However, key risk factors require acknowledgment:

- Solana's weekly x402 transaction count dropped from 6.8M in December 2025 to approximately 510,000 in February 2026, a 90% decline from peak.

- Data indicates that 78% of peak-period transactions were classified as non-organic (test activity, bot transactions, or incentive-driven volume).

Agentic payments at this stage should be characterized as an option value, not a realized revenue driver. Its ultimate worth depends on whether the AI agent economy scales materially, and whether, when it does, on-chain micropayments become the preferred settlement layer over traditional API billing. Solana's technical fit is strong; organic demand validation remains early-stage.

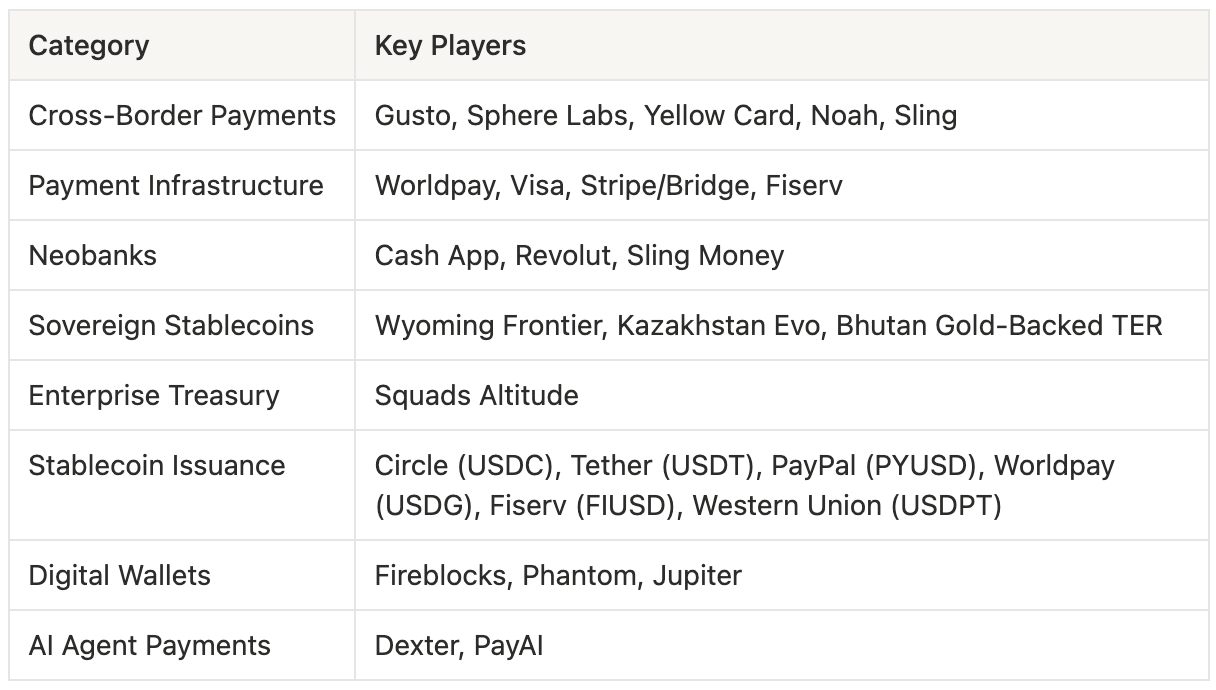

VIII. Ecosystem Overview: Building Blocks of Solana's Payment Infrastructure

Solana's payments ecosystem has developed across a complete set of verticals:

One signal merits particular attention: sovereign-backed stablecoins are beginning to appear on Solana. Wyoming, Kazakhstan, and Bhutan have each issued or formally announced plans to issue stablecoins with sovereign backing on Solana. This represents institutional recognition at the nation-state level, a qualitatively different category of endorsement than commercial partnerships.

IX. Investment Framework: Evaluating Solana's Payments Thesis

Solana's payments narrative reflects four years of deliberate strategic accumulation, spanning from Solana Pay to payments.org, from Shopify integration to Visa settlement, from PYUSD to USDPT. Each step has moved the chain further from a retail-driven trading network toward institutional-grade financial infrastructure.

Three core conclusions emerge from the evidence.

1. Technical performance is the entry requirement. Institutional trust is the moat.

Sub-second confirmations, sub-cent fees, and 100M+ daily transaction capacity place Solana on the consideration set for payment infrastructure. What has driven it to its current position is four years of systematic institution-building: regulatory frameworks, compliance tooling, and bilateral relationships developed with major financial counterparties.

The collective deployment by Visa, PayPal, Stripe, Western Union, and Fiserv delivers more than transaction volume. It creates institutional credibility that functions as a compounding signal. When a 165-year-old remittance institution (Western Union) issues a stablecoin on Solana, the signaling effect on other financial institutions materially exceeds the direct transaction value.

2. Solana and Tron are not competing in the same market.

Tron's dominance in emerging-market USDT remittances is built on lowest fees and broad grassroots distribution, a position reinforced by deeply entrenched user behavior that is difficult to displace. Solana is competing for institutional stablecoin settlement, enterprise treasury on-chain migration, and AI agent payment infrastructure — incremental markets with almost no overlap in user profile, technical requirements, or compliance framework.

3. The central question is whether organic demand materializes at scale.

Retail payment penetration is approximately 1% of total volume. Agentic payment metrics contain significant non-organic activity. Solana does not register as a major factor in mainstream global stablecoin payment flows. The institutional partner roster is strong, but whether these partnerships convert into sustained, scalable, organic transaction volume remains the open question that will determine the long-term thesis.

Key metrics to monitor:

- Institutional partnership depth: Is Visa migrating incremental settlement volume to Solana? What are actual adoption rates following Western Union USDPT's full rollout?

- Cross-border payment application growth: User and transaction volume trends at Zepz, BVNK, Gusto, and comparable partners

- Agentic payments organic validation: Are mainstream AI applications adopting x402 at scale, and what share of activity is demonstrably non-incentivized?

Solana's structural advantages, technical performance and institutional-grade compliance tooling, are well-established. The unanswered question is whether those advantages translate into real, sustained, organic payment flows.

The trajectory of these three metrics will determine whether Solana's payments transformation represents a durable identity shift — or a well-constructed institutional narrative awaiting fundamental validation.

Data sources: Artemis Analytics, Visa Onchain Analytics, CoinGate Annual Report, Messari, Grayscale Research, Solana Foundation, payments.org, company public disclosures. All figures as of March 2026 unless otherwise noted.

Enjoyed this article?

Subscribe to 168X on Substack for our latest deal flow and research.